Rural Providers Are Dreaming Big, But Not Acting Big.

Our third survey of rural healthcare providers yielded many interesting insights about their challenges, IT use and wish list. Deciphering the results from our more than 150 rural healthcare respondents yielded perhaps the most important finding of all – rural providers are eager for technology advancement but they are not taking the necessary steps to make that vision a reality. In this report you’ll learn:- Top seven factors preventing rural healthcare organizations from technology adoptions or upgrades

- Rural provider growth plans for the next five years

- Three top trends for rural providers in 2019

- Organic growth

- Enhanced capabilities in patient monitoring and care

- Improved profitability

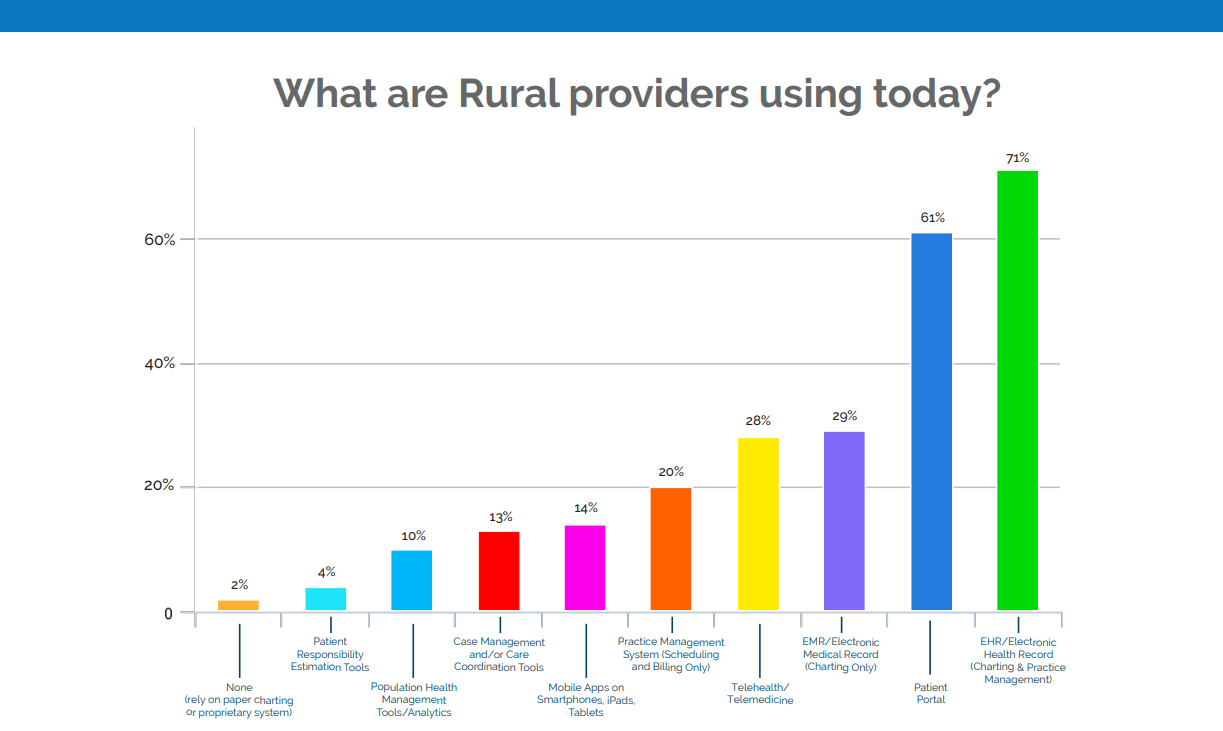

The desire for mobile apps is particularly strong among independent primary care and specialty clinics (44%), while critical access hospitals are especially interested in patient responsibility estimation tools (25%).

The desire for mobile apps is particularly strong among independent primary care and specialty clinics (44%), while critical access hospitals are especially interested in patient responsibility estimation tools (25%).

This is the 3rd consecutive survey where cost topped the obstacles preventing new technology adoption or IT upgrades. (Surveys are conducted every other year.)

But while cost continues to be the #1 obstacle —by a 24% margin—so are lack of staffing and IT resources, uncertainty around benefits and ROI of new technologies, and concerns around integrating new technologies into existing workflows.

For critical access hospitals in particular, the smaller the hospital, the more likely staffing, recruitment, and retention were to be cited as barriers to technology adoption.

This is the 3rd consecutive survey where cost topped the obstacles preventing new technology adoption or IT upgrades. (Surveys are conducted every other year.)

But while cost continues to be the #1 obstacle —by a 24% margin—so are lack of staffing and IT resources, uncertainty around benefits and ROI of new technologies, and concerns around integrating new technologies into existing workflows.

For critical access hospitals in particular, the smaller the hospital, the more likely staffing, recruitment, and retention were to be cited as barriers to technology adoption.

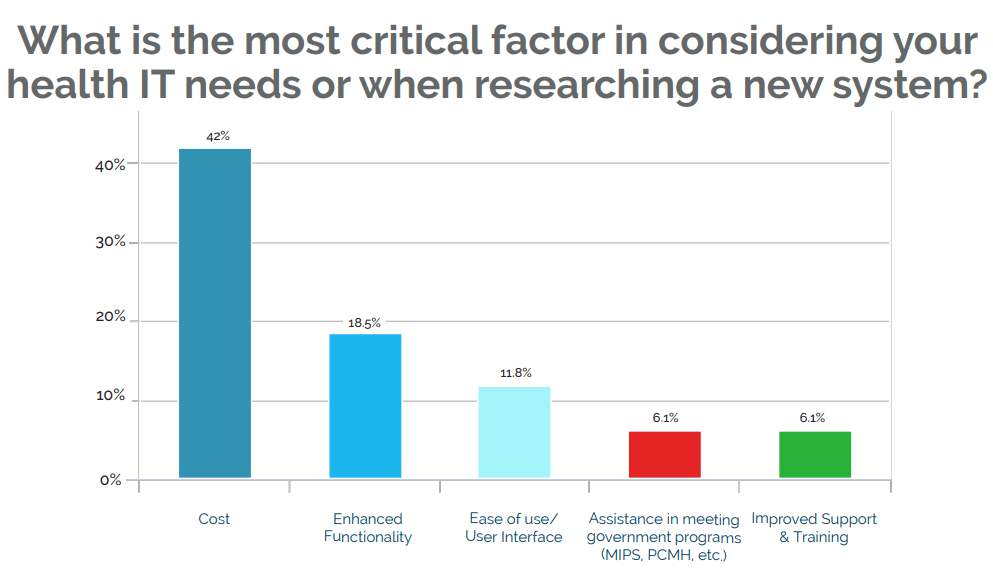

Not only is cost the number one barrier to adoption, it is also the most critical factor rural providers evaluate in researching new systems. The wide gap between this factor and the second-highest consideration, “enhanced functionality,” is notable.

The prevalence of inaction resulting from lack of information or fear stalls rural providers’ efforts to achieve their vision.

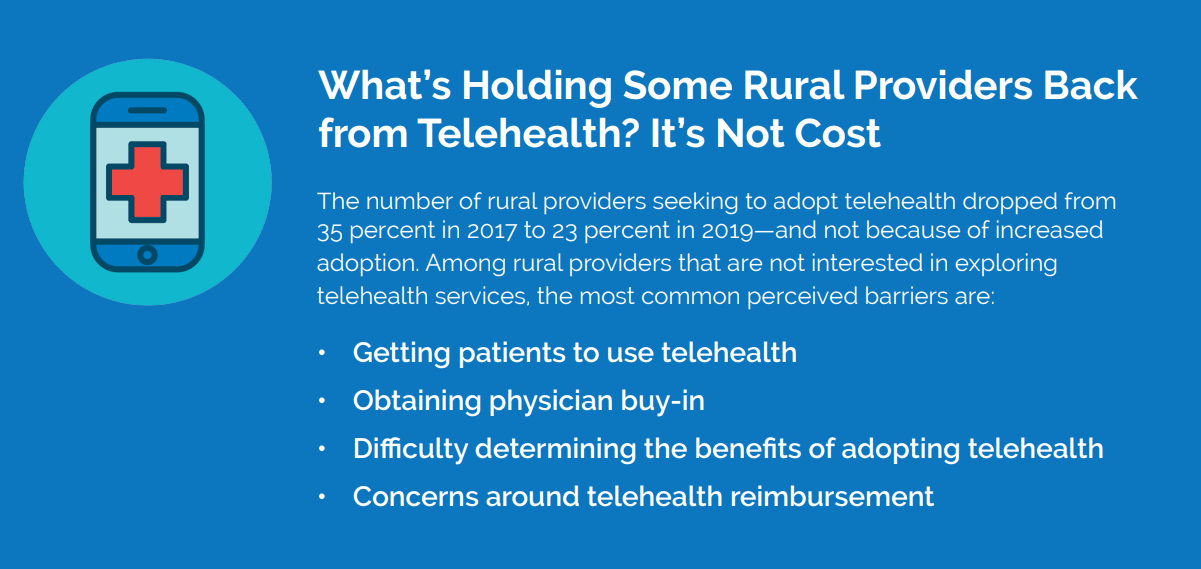

For example, just 22% of rural healthcare respondents plan to change their technology solutions, down from 43% in 2017—even when some services or tools, such as telehealth, are reimbursed by commercial and government insurers or have the potential to strengthen providers’ financial performance.

Not only is cost the number one barrier to adoption, it is also the most critical factor rural providers evaluate in researching new systems. The wide gap between this factor and the second-highest consideration, “enhanced functionality,” is notable.

The prevalence of inaction resulting from lack of information or fear stalls rural providers’ efforts to achieve their vision.

For example, just 22% of rural healthcare respondents plan to change their technology solutions, down from 43% in 2017—even when some services or tools, such as telehealth, are reimbursed by commercial and government insurers or have the potential to strengthen providers’ financial performance.

- 56% of rural providers did not participate in a value-based payment (VBP) program in 2018

- 35% were unsure whether they would participate in a quality reporting program in 2019, or did not plan to do so

- 25% said their primary barrier to participation in VBP programs is lack of knowledge around which programs are available or best fit their practice

- 44% cited lack of resources or training as their top barrier

Top 3 Trends For Rural Healthcare Providers

Trend #1: Identifying and overcoming reimbursement obstacles is necessary for rural providers to achieve their vision for care and service in their communities.

- The Azalea Health survey shows that 48 percent of rural providers consider declining reimbursements to be their biggest challenge. As Medicare and others in the payer mix increasingly move from fee-forservice payment to value-based payment (VBP) models, it’s clear that strengthening capabilities for value-based performance is key to organizations’ financial health. Yet few rural providers are taking action:

- Just 44 percent of rural providers participated in a VBP program in 2018, and nearly 35 percent were unsure whether they would participate in a quality reporting program in 2019 or did not plan to do so.

- Twenty-seven percent of rural providers say their primary barrier to participation in VBP programs is lack of knowledge around which programs are available or best fit their practice. This is especially true among independent rural health clinics (43 percent).

- Another 44 percent of rural providers say they don’t have the training or staff to participate in quality reporting programs.

Trend 2: Mastering the psychology of patient behavior will be key to rural providers’ ability to improve performance on multiple levels.

Patient engagement—both patient financial engagement and engagement in managing chronic conditions—will be key to rural providers’ success in 2019.

With senior leaders ranking declining reimbursement as their top challenge, strengthening the ability to collect patient copays and out-of-pocket balances should be a top priority. So should investments in training and technologies that more effectively help patients take ownership for managing chronic and costly conditions.

When these conditions are not managed appropriately, this can increase hospital admissions and readmission rates, which in turn impact reimbursement.

Patient financial engagement

A common pain point for 35 percent of rural healthcare facilities surveyed is difficulty collecting from patients. At a time when nearly half of all rural hospitals are operating with negative operating margins, patient financial engagement is a necessary component for strengthening financial performance and boosting cash flow.

When staff avoid conversations around out-of-pocket costs for care, patients are more likely to forgo needed care, shop for healthcare services elsewhere, or respond angrily when bills do arrive. Waiting to have these discussions until after the patient has left the facility is also detrimental to a rural facility’s financial health.

One McKinsey study found collection rates significantly decrease after the patient visit, with providers collecting just 50 to 70 percent of the balance, on average.

However, when front-office staff master the psychology of patient behavior at the point of service, they are better positioned not only to collect copays, but also to have meaningful discussions around the patient’s total out-of-pocket cost of care. Staff then feel more empowered to request the balance in full—and patients are more likely to respond, even by paying a portion and agreeing to a payment plan.

A transparent patient financial services process is one factor that can change the psychology of patient payment. Leading healthcare organizations are increasing transparency around patient financial communications and equipping their financial services staff with the skills and the resources to compassionately and effectively lead patients through the payment process.

A transparent patient financial services process is one factor that can change the psychology of patient payment. Leading healthcare organizations are increasing transparency around patient financial communications and equipping their financial services staff with the skills and the resources to compassionately and effectively lead patients through the payment process.

These include:

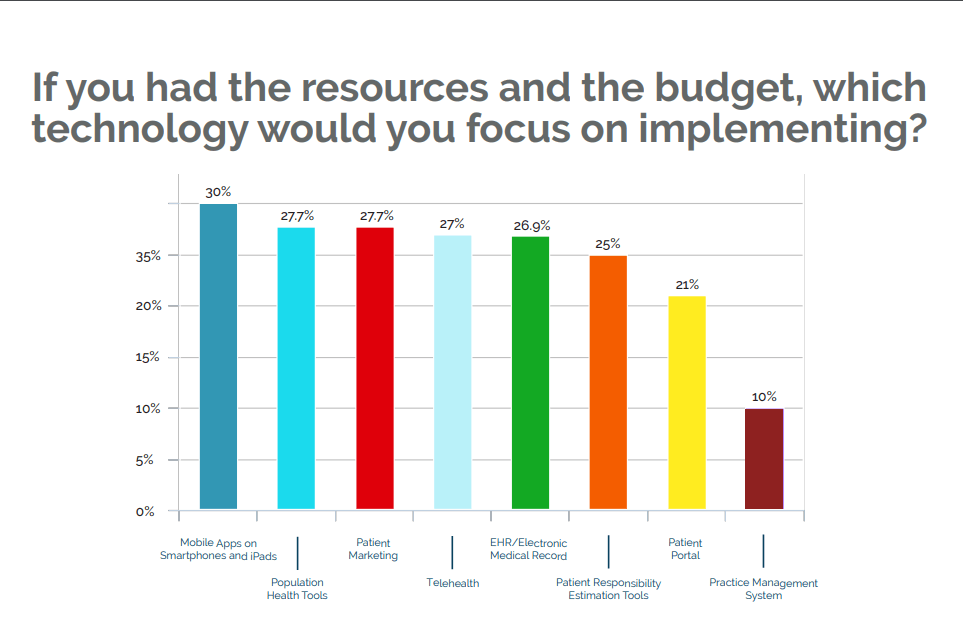

- Patient responsibility estimation tools, desired by 26 percent of rural providers surveyed

- Tools that predict a patient’s propensity to pay

- Financial assistance screening tools

Providing an estimate that is specific to the individual is a differentiator between “good” and “great” communication. So is putting price information in context with the quality and safety of care the facility provides.

Offering multiple options for payment, including mobile payment, also is critical. Additionally, providers should have processes in place to help patients who may qualify for outside assistance.

It could also point to alternative opportunities for improving population health that may make more sense for the organization given its staffing, technological capabilities, and resources. Additionally, careful review of existing technologies could point to entryways to population health management that complement existing workflows and make financial sense for the organization.

Ultimately, research and preparation will differentiate those organizations that know their appetite for risk from those that are continually following the crowd.

It could also point to alternative opportunities for improving population health that may make more sense for the organization given its staffing, technological capabilities, and resources. Additionally, careful review of existing technologies could point to entryways to population health management that complement existing workflows and make financial sense for the organization.

Ultimately, research and preparation will differentiate those organizations that know their appetite for risk from those that are continually following the crowd.

3 Strategies For Rural Healthcare Success

For rural providers to “act big” on their vision, they must arm themselves with the knowledge needed to overcome fears and misconceptions, change patient behavior, and elevate quality and financial performance.#1. Take Action To Ensure Your Financial Future

With nearly half of rural hospitals operating under negative margins, rural healthcare organizations can’t afford to operate from a place of skepticism when it comes to making decisions that could impact reimbursement, such as quality program participation or investment in new services. Moving from big vision to big action requires that rural healthcare providers take the time to:- Investigate which quality programs are best suited to their organization—and develop action plans for testing the waters.

- Understand the ways in which changes in reimbursement could propel investments in technologies that could make a big impact on patient health, efficiency, cost, and more.

- Talk with other rural healthcare organizations about how they’ve dealt with common challenges—and seek to apply the lessons learned

#2 Revamp Your Approach to Patient Engagement

Effectively engaging patients in their care can lead to improved quality, safety and efficiency. It can also reduce costs and elevate performance under VBP models, increasing reimbursement. Look for ways to more effectively engage patients at each stage in their care journey. Now may be the time to move mobile health apps from wish lists to reality for chronic care patients to move the needle on quality performance. Look at your 30-day readmission stats to determine whether incorporating mobile apps for care management could make a difference for specific types of patients—and generate the ROI needed to justify this innovation. Software vendors sometimes provide ROI analyses based on past performance to make the process easier for you. It’s also important to consider ways to more effectively engage patients in taking financial responsibility for their care. Consider providing front-office staff with scripting that mirrors these best practices from the Healthcare Financial Management Association:- Avoid surprises. Let patients know what to expect, including the potential for physician fees that are separate from the estimate provided.

- Find out whether patients will need assistance paying their bill.

- Communicate directly—cut to the chase.